Market Perspective - Spring 2026

- Adam Schacter

- Apr 8

- 11 min read

Guide to the markets

Sifting through financial information online is becoming quite onerous with so many opinions out there, so we've consolidated what we believe to be informative and insightful into one Market Commentary.

This Commentary includes:

Avesta Wealth NP Ascension Growth Portfolio

Avesta Wealth NP Private Assets Pool

Q2 2026 Market Commentary: A Global Economy Finding Its Balance

This commentary summarizes thoughts from Dr. David Kelly, a highly respected macroeconomist from JP Morgan, and provides graphs and tables to provide context and support.

If the first quarter of 2026 felt unsettling, it’s because it was unsettling.

Geopolitical tensions escalated, energy prices moved sharply higher, and markets continued to concentrate around a relatively small group of companies. It’s the kind of environment that can make the global economy feel fragile.

But stepping back, I think the more accurate description is not fragility—it’s transition.

We seem to be moving through a period where the drivers of growth, inflation, and market returns are shifting. And while that creates short-term noise, it doesn’t change the longer-term foundation.

One of the most visible developments this year has been the rise in oil prices following conflict in the Middle East. Energy markets are global by nature, so these effects are being felt broadly—from North America to Europe to Asia. Higher fuel and transportation costs tend to work their way into inflation quickly, and we may see global inflation readings move modestly higher through the middle of this year.

But the impact is uneven. Energy-exporting regions—such as parts of North America and emerging markets—benefit from higher oil prices, while energy-importing economies, particularly in Europe and parts of Asia, feel more of the strain. This divergence is important, because it means the global economy is not moving in lockstep. Some regions are being supported, while others are being pressured.

At the same time, a larger and more structural shift is unfolding across developed economies: slower population growth.

In many parts of the world, aging populations and lower immigration are reducing the growth of the workforce. This naturally limits how fast economies can expand. But offsetting this is a steady rise in productivity, driven by technology, automation, and increasingly, artificial intelligence.

Globally, we’re seeing the same pattern repeat itself: fewer workers, but more output per worker.

The result is likely a world of more moderate, but still stable, economic growth. Rather than the faster expansions of previous decades, many developed economies may settle into a range closer to 1.5%–2%, with emerging markets continuing to grow faster.

In the near term, growth is likely to be uneven rather than weak.

Some economies should see temporary support from fiscal measures and consumer spending, while others will slow as policy tightens or external pressures build. This kind of unevenness is typical in a global cycle—and it often creates opportunities as different regions move at different speeds.

Labour markets globally reflect this same balance.

Hiring has slowed in many regions, but unemployment remains relatively low. In part, this is because the supply of workers is no longer growing the way it once did. At the same time, businesses seem to be acting more cautious, choosing to manage costs rather than aggressively expand. This has kept wage growth relatively contained, which is an important factor in preventing inflation from becoming entrenched.

As for inflation, while we may see some near-term upward pressure, the broader trend still suggests moderation.

Energy-driven inflation spikes tend to be temporary. Meanwhile, housing costs—which have been a major contributor to inflation globally—are beginning to stabilize in many markets. As these forces play out, inflation seems likely to ease again into 2027.

Central banks are responding accordingly. While markets had anticipated a more aggressive shift toward lower interest rates in 2026, policymakers are taking a more cautious approach. With growth holding up and inflation not yet fully settled, most major central banks appear willing to wait. Rate cuts may come—but likely later, and more gradually than previously expected.

From an investment perspective, this environment is leading to a broader rebalancing across markets.

U.S. equities remain a dominant force, particularly at the large-cap level, where a small number of companies continue to drive a disproportionate share of returns. These businesses are strong, but their valuations reflect a great deal of optimism, and market leadership has become increasingly concentrated.

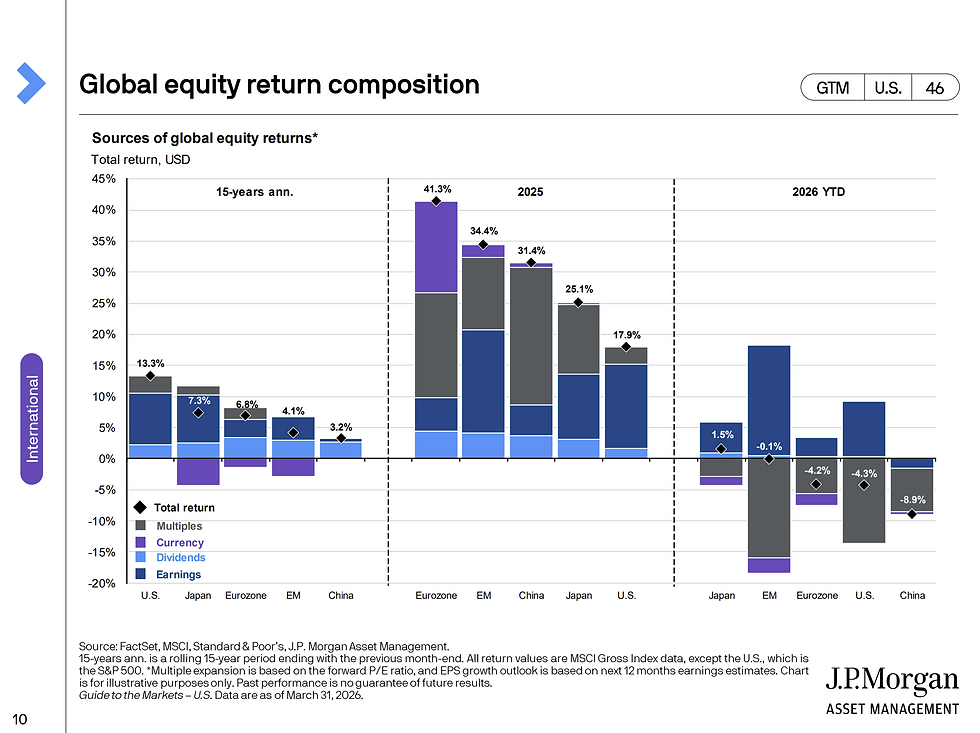

At the same time, international markets—both developed and emerging—continue to trade at more moderate valuations. Over the past year, they have quietly begun to perform more competitively, supported in part by currency movements and in part by improving fundamentals. For many investors, this represents a shift worth paying attention to, particularly after a long period of U.S. dominance.

Another notable trend is the growing role of alternative investments.

In a world where both stocks and bonds have been influenced by inflation and interest rate changes, investors are increasingly looking for additional sources of return, income, and diversification. Assets such as infrastructure, private credit, and real estate can play different roles within a portfolio—some providing stability, others offering exposure to long-term growth themes like energy systems and digital infrastructure.

They are not without complexity, and they require a long-term perspective, but their role in portfolios continues to expand.

Ultimately, what ties all of this together is the importance of balance.

After several strong years in markets, many portfolios today are larger—but also more concentrated and, in some cases, carrying more risk than originally intended. At the same time, the global backdrop remains uncertain, not because the system is fragile, but because it is evolving.

This is exactly the kind of environment where discipline matters most.

Not reacting to headlines. Not chasing what has already performed. But instead maintaining a thoughtful, diversified approach that reflects both the opportunities and the risks across global markets.

That has always been the foundation of long-term investing—and it remains just as relevant today.

The Market Insights program provides comprehensive data and commentary on global markets without reference to products. Designed as a tool to help clients understand the markets and support investment decision-making, the program explores the implications of current economic data and changing market conditions.

J.P. Morgan Asset Management Market Insights and Portfolio Insights programs, as non-independent research, have not been prepared in accordance with legal requirements designed to promote the independence of investment research, nor are they subject to any prohibition on dealing ahead of the dissemination of investment research.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction, nor is it a commitment from J.P. Morgan Asset Management or any of its subsidiaries to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical and for illustration purposes only. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their personal goals. Investors should ensure that they obtain all available relevant information before making any investment. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

J.P. Morgan Asset Management is the brand for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide.

To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our privacy policies.

Portfolio Updates

The introduction of our Growth Pool and Private Assets Pool as core holdings reflects a broader evolution in how we are building portfolios—focused on improving diversification, reducing costs, and expanding access to high-quality investments.

The Avesta Wealth NP Ascension Growth Portfolio is designed to be the core engine of long-term returns, providing broad global equity exposure with a more balanced structure than traditional indices. By tilting toward international markets and incorporating equal-weight strategies, it reduces reliance on a small group of mega-cap companies while maintaining full participation in global growth. It also allows us to efficiently hold smaller, high-quality positions that would otherwise be difficult to implement at the individual account level, all within a cost-conscious structure.

While still early, this approach has already helped provide relative resilience, with the portfolio moderately elevated during a period where broader markets have seen declines.

Feature Holding - Invesco S&P 500 Equal Weight ETF (EQL)

The Invesco S&P 500 Equal Weight ETF (EQL) offers a different way to access the U.S. equity market. Unlike traditional index funds that are heavily weighted toward the largest companies, EQL gives each company in the S&P 500 an equal allocation. This results in broader exposure across sectors and company sizes, reducing reliance on a small group of mega-cap stocks that have increasingly dominated market returns in recent years.

Within the Growth Portfolio, EQL plays an important balancing role. It maintains full participation in U.S. equities, while improving diversification and reducing concentration risk. It also introduces a natural tilt toward mid-sized companies and value-oriented segments of the market, which have historically performed well over longer cycles, particularly when market leadership broadens. For investors, this creates a more balanced and resilient way to capture U.S. growth—one that is less dependent on a handful of companies and better positioned for a wider range of market environments.

You can learn more about the Avesta Wealth NP Ascension Growth Portfolio HERE, which includes a tool to see the allocated portfolio selections held inside it, and links for more information on each holding.

The Avesta Wealth NP Private Assets Pool is designed to complement traditional portfolios by providing access to investment opportunities that are typically unavailable in public markets. It focuses on high-quality private assets—such as real estate, infrastructure, private equity, and private credit—that can generate consistent income and enhance overall portfolio stability. These investments are often less sensitive to day-to-day market volatility, allowing them to provide a smoother return profile while still delivering attractive long-term results.

Equally important, the pooled structure allows investors to access institutional-caliber managers and diversified private investments at a scale that would otherwise be difficult to achieve individually. This not only improves diversification within the private asset space, but also helps reduce costs and improve overall efficiency. While these investments are less liquid and require a longer-term mindset, they play a valuable role in strengthening portfolios—adding income, diversification, and resilience in a way that traditional stocks and bonds alone often cannot.

Feature Holding – Yorkville Health Care Fund

The Yorkville Long-Term Healthcare Fund is designed to provide investors with exposure to one of the most durable and structurally supported areas of the economy: healthcare services. With aging populations across North America and globally, demand for long-term care, senior housing, and specialized medical services continues to grow steadily, largely independent of economic cycles. This creates a unique investment opportunity—one that combines stable, needs-based demand with the potential for consistent income and long-term capital appreciation.

Within a portfolio, this fund plays an important diversifying role. Its returns are driven less by market sentiment and more by underlying demographic trends and contractual cash flows, which can help reduce overall volatility. At the same time, by investing through an experienced manager with a focused strategy, the fund provides access to a specialized segment of private markets that would be difficult to replicate individually. For long-term investors, it offers a compelling combination of resilience, income generation, and exposure to a sector with strong secular tailwinds; and with tax efficiency, allowing you to keep more of what you earn.

You can learn more about the Avesta Wealth NP Private Assets Pool HERE, which includes a tool to see the allocated portfolio selections held inside it, and links for more information on each holding.

Changes to the Portfolio

We will use this section to outline changes within each of the pools, as well as track progress going forward. We don't yet have a relevant history to draw on in this section, and so for now, we can include some key details about the new Pools:

Liquidity and Net Asset Value.

Changes to the Growth Pool's Net Asset Value (NAV) are based on audit of the underlying holdings, and occur weekly at the end of every Monday. The new NAV is reviewed on Tuesday, and the price change of the Pool shows updated in client accounts on Wednesdays. Liquidity for this Pool is offered weekly.

Audit of the Private Asset Pool's NAV occur monthly at the end of each month. The new NAV is reviewed the next day, and the price change of the Pool shows updated in client accounts the day after. Liquidity for this Pool is offered monthly.

Reporting

We aim to provide an improvement to our current reporting system, and this process is partially underway.

You can review a breakdown of each Pool's allocation, and details of each investment holding within each of the Pools using the tools on our website. This allows you to access exactly (to the penny) what you are invested in at any given time, as well as links to resources to learn more about each holding - something that was not offered prior to the advent of these Pools.

The Private Assets Pool contains some holdings that we are working to divest from (illiquid), and so it will take time to get this Pool to where we would like it to be. There is nothing fundamentally wrong or untoward about its makeup at current, but we want to be more deliberate about how we go about allocating, and it will just take a bit of time to get there.

We're still in the process of launching a supplemental portal called NDex that will provide clearer and more robust reporting on performance and other investment metrics. We are hoping the launch of this system occurs in April and are working to ensure it is in proper order in advance of offering it to you.

The Market Commentary (this market commentary) will continue to be presented to you each quarter, but it will be more tailored towards how the macroeconomic environment has led to changes to your portfolio, and why. I trust this will be a welcomed communication going forward as we outline what we have done, and why we think this will be impactful to you and your objectives of growing and preserving wealth.

We continue to monitor any potential new holdings on an almost daily basis, and continue to evaluate your existing holdings to determine if the reasons we bought them in the first place remain true today.

We hope you find this both interesting and informative in keeping pace with the events of today’s financial world.

This publication contains the opinions of the writer. The information contained herein was obtained from sources believed to be reliable, but no representation or warranty, express or implied, is made by the writer, Designed Securities Ltd. or any other person as to its accuracy, completeness or correctness. This publication is not an offer to sell or a solicitation of an offer to buy any securities. The information in this publication is intended for informational purposes only and is not intended to constitute investment, financial, legal, tax or accounting advice. Many factors unknown to us may affect the applicability of any statement or comment made in this publication to your particular circumstances. Hence, you should not rely on the information in this publication for investment, financial, legal, tax or accounting advice. You should consult your financial advisor or other professionals before acting on any information in this communication.

Avesta Wealth is an investments trade name of Designed Securities Ltd (DSL). DSL is regulated by the Canadian Investment Regulatory Organization (www.ciro.ca) and Member of the Canadian Investor Protection Fund (www.cipf.ca ). Investment products are provided by Designed Securities Ltd. and include, but are not limited to, mutual funds, stocks, and bonds. Adam Schacter is registered to provide investment advice and solutions to clients residing in the provinces of British Columbia, Alberta, Manitoba, Ontario, Quebec, and Nova Scotia.

Comments